Can Spread Duration Be Negative . a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. spread duration is the sensitivity of a security’s price to changes in its credit spread. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or dv01 in the united. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. It will be a poor performer as the yield curve steepens. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. A security’s credit spread is the.

from analystprep.com

in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. spread duration is the sensitivity of a security’s price to changes in its credit spread. A security’s credit spread is the. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or dv01 in the united. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. It will be a poor performer as the yield curve steepens.

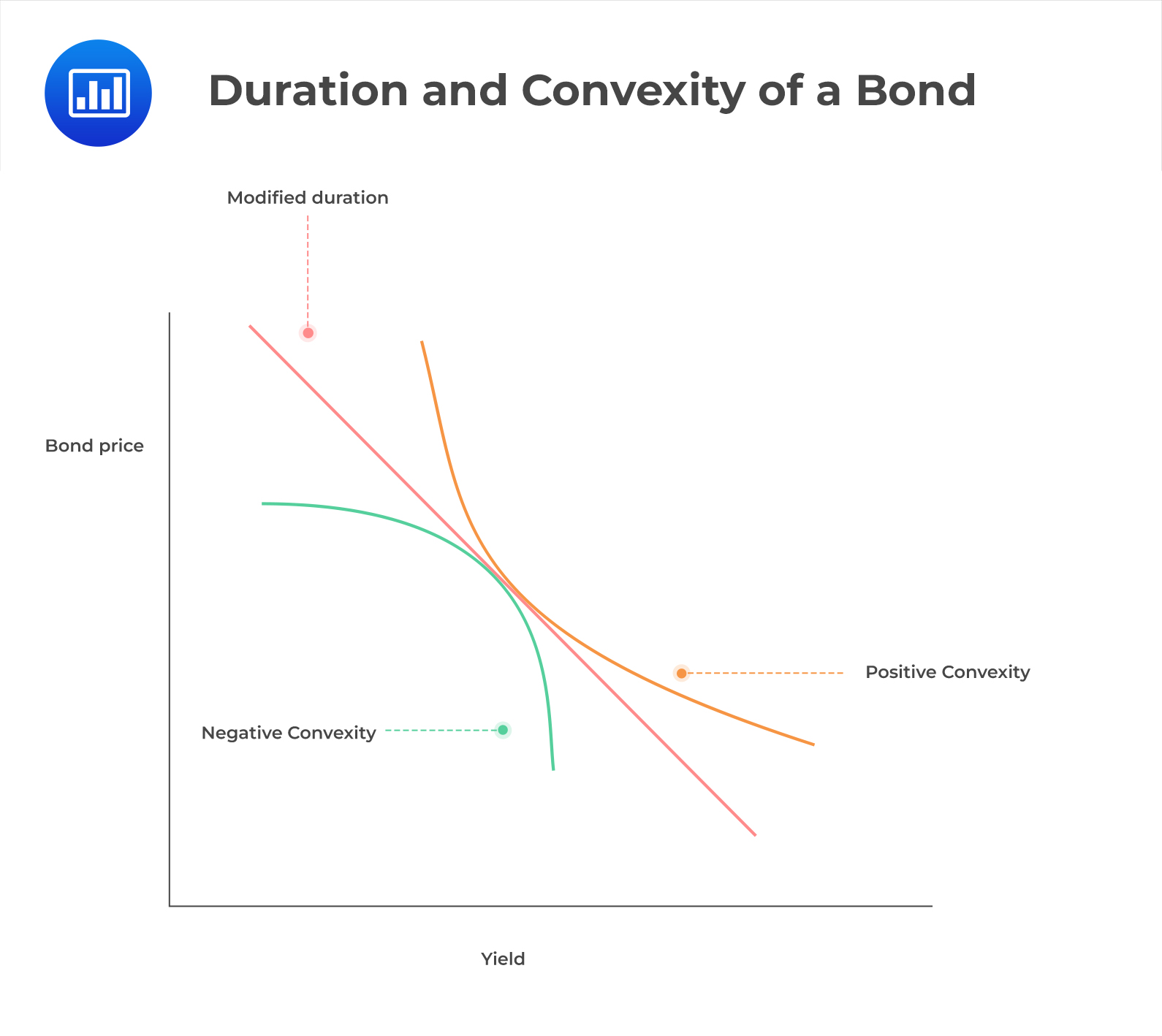

Exposure Measures and Their Use CFA, FRM, and Actuarial Exams Study Notes

Can Spread Duration Be Negative the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or dv01 in the united. A security’s credit spread is the. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. It will be a poor performer as the yield curve steepens. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or dv01 in the united. a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. spread duration is the sensitivity of a security’s price to changes in its credit spread. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Can Spread Duration Be Negative in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. the basic rule of thumb for using duration says that for every percentage point that. Can Spread Duration Be Negative.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Can Spread Duration Be Negative a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or dv01 in the united. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Chapter 6 PowerPoint Presentation, free download ID4021126 Can Spread Duration Be Negative A security’s credit spread is the. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. spread duration is a key metric used by. Can Spread Duration Be Negative.

From www.chegg.com

Solved A Negative Charge Q Is Spread Uniformly Along Th... Can Spread Duration Be Negative in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation ID3950949 Can Spread Duration Be Negative the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. spread duration is the sensitivity of a security’s price to changes in its credit. Can Spread Duration Be Negative.

From www.westernsouthern.com

An Innovative Approach to Measuring Spread Risk Can Spread Duration Be Negative spread duration is the sensitivity of a security’s price to changes in its credit spread. A security’s credit spread is the. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. in contrast to the more typical positive duration, a “negative” duration strategy can be. Can Spread Duration Be Negative.

From analystprep.com

Exposure Measures and Their Use CFA, FRM, and Actuarial Exams Study Notes Can Spread Duration Be Negative the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. It will be a poor performer as the yield curve steepens. a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. A security’s credit spread is the.. Can Spread Duration Be Negative.

From www.chegg.com

Solved (6) Problem 9 A point charge, Q1 = 5.2 uC, is Can Spread Duration Be Negative It will be a poor performer as the yield curve steepens. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. spread duration is the sensitivity of a security’s price to changes in its credit spread. the basic rule of thumb for using duration says that. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Managing Interest Rate Risk(II) Duration GAP and Economic Value Can Spread Duration Be Negative the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. A security’s credit spread is the. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. the money duration, or basis point value or. Can Spread Duration Be Negative.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Can Spread Duration Be Negative a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. spread duration is the sensitivity of a security’s price to changes in its credit spread. the. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Can Spread Duration Be Negative A security’s credit spread is the. spread duration is the sensitivity of a security’s price to changes in its credit spread. It will be a poor performer as the yield curve steepens. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. the money duration, or. Can Spread Duration Be Negative.

From www.chegg.com

Solved (5\) Problem 17 A negative point charge, Q1, is Can Spread Duration Be Negative A security’s credit spread is the. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. spread duration is the sensitivity of a security’s. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Can Spread Duration Be Negative It will be a poor performer as the yield curve steepens. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. spread duration is the sensitivity of a security’s price to changes in its credit spread. a negative basis indicates a broader yield spread than. Can Spread Duration Be Negative.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Can Spread Duration Be Negative A security’s credit spread is the. spread duration is the sensitivity of a security’s price to changes in its credit spread. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. a negative basis indicates a broader yield spread than the cds, while a positive basis. Can Spread Duration Be Negative.

From www.financestrategists.com

Spread Duration Definition, Components, & Applications Can Spread Duration Be Negative spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. It will be a poor performer as the yield curve steepens. a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. A security’s credit spread is the. Web. Can Spread Duration Be Negative.

From www.slideserve.com

PPT Duration times spread PowerPoint Presentation, free download ID Can Spread Duration Be Negative a negative basis indicates a broader yield spread than the cds, while a positive basis suggests a tighter yield. spread duration is a key metric used by bond investors to assess the sensitivity of a bond’s price to changes in. the money duration, or basis point value or bloomberg risk [citation needed], also called dollar duration or. Can Spread Duration Be Negative.

From www.pzacademy.com

spread duration有问必答品职教育 专注CFA ESG FRM CPA 考研等财经培训课程 Can Spread Duration Be Negative in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a very. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. spread duration is a key metric used by bond investors to assess the sensitivity. Can Spread Duration Be Negative.

From freefincal.com

Term spread as a macroeconomic indicator Can Spread Duration Be Negative spread duration is the sensitivity of a security’s price to changes in its credit spread. the basic rule of thumb for using duration says that for every percentage point that rates move up or down, a bond. in contrast to the more typical positive duration, a “negative” duration strategy can be employed by a manager with a. Can Spread Duration Be Negative.